Haranga Resources (ASX:HAR)

Haranga Resources (ASX:HAR)

African Uranium: Could Saraya be the next Etango?

Speculating in exploration stocks is wild.

Only a select few are winners, and many are lifestyle companies that wipe out your capital while moving from one shiny object to another. Buying in cheap into microcaps is easy. Buying in cheap into something real and (potentially) valuable is difficult.

Earlier this week I published a post with all of the uranium companies on the ASX that I could find with a market cap of less than $50m, with a high level summary of each company…

Haranga Resources (ASX:HAR) caught my attention as I was compiling that post. They have a resource, are doing methodical exploration of it (and surrounds), and they appeared to have a team with a track record of success. All this for a market cap of $13.2m.

So, if you’d like to spend a few minutes wrapping your head around Haranga, read on!

Disclaimer: This is not financial advice, and I am not a financial advisor.

Contents

Chart

Financials

People

Projects

Where to from here?

Haven’t subscribed yet? Get free posts to your email at least once a week with deep dives into microcap stocks that might just have something to them.

Know someone who shares your passion for microcap stocks? Do them (and me!) a favour and send this post their way!

Chart

The first thing we notice about Haranga is that its chart doesn’t go back that far, and that it’s quite thinly traded. Oscillating between 10c and ~20-25c, it is currently 14c, towards the bottom of its historical range.

Financials

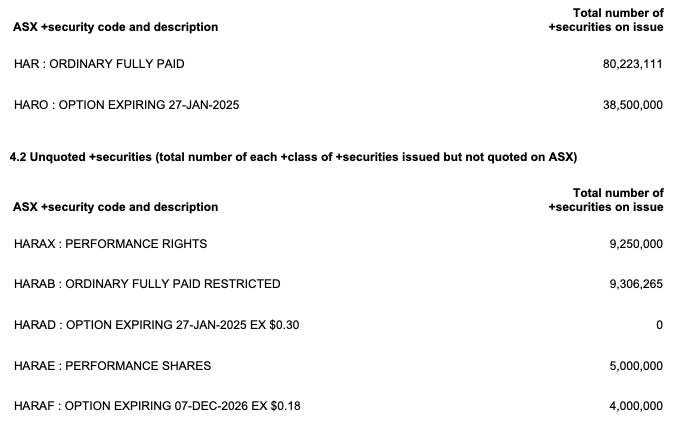

Shares on Issue/Market Cap

Haranga has 94.5m shares on issue (I’m including HAR, HARAB and HARAE below). There are 4m options that are in the money at 18c and another 38.5m that are in the money at 30c - these are listed as HARO.

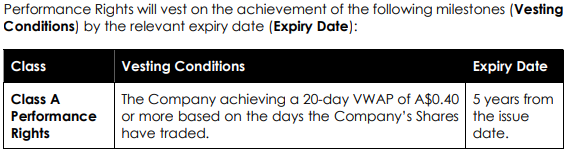

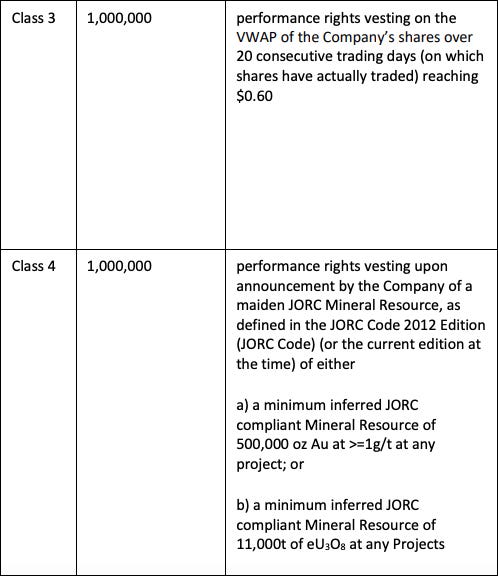

Details of performance rights are below. Note that Class C has already vested with the release of the JORC resource in September.

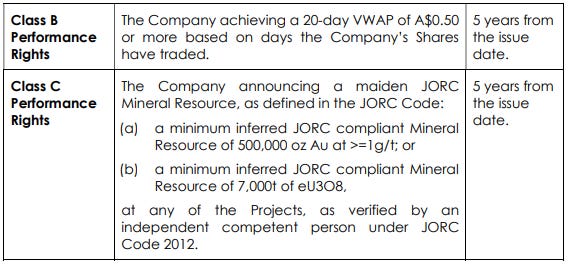

These are the targets for new MD Peter Batten, who has 4m Performance Rights vesting after 5 years:

Cash

The company had $1.95m in the bank on the 31/12/2023. That was 2.43 quarters left of runway based on the December quarter’s spend rate.

People

Peter Batten

Having joined only in September last year, this is the man who staked Bannerman’s ground in Namibia in 2006 and had defined over 100Mlb at Etango by the time he departed in 2009.

Raiden Resources Connections: Michael Davy, Kyla Garic, Dusko Ljubojevic

Non-Exec Chair Michael Davy and Company Secretary Kyla Garic hold the same respective roles at Raiden Resources (ASX:RDN), whose MD Dusko Ljubojevic is a substantial holder of Haranga (not otherwise involved), holding ~6% of the company.

After Azure Minerals’ (ASX:AZS) Andover lithium find in the Pilbara, RDN searched their own tenements for lithium next door, leading to a 26x share price move from 0.3c to 8c - since retraced to 2.3c.

I believe the connection between the two companies is a positive on the whole - Raiden was quick to pick up land adjoining Azure’s project after their discovery and seems to have a pragmatic approach to corporate activity. While Ljubojevic is not involved directly with Haranga, with Batten as MD, there’s a strong argument that for the task at hand - expanding an African uranium resource - the company is well led.

Projects

Saraya Uranium Project (HAR - 70% / Mandinga Resources 30%, free carried to PFS)

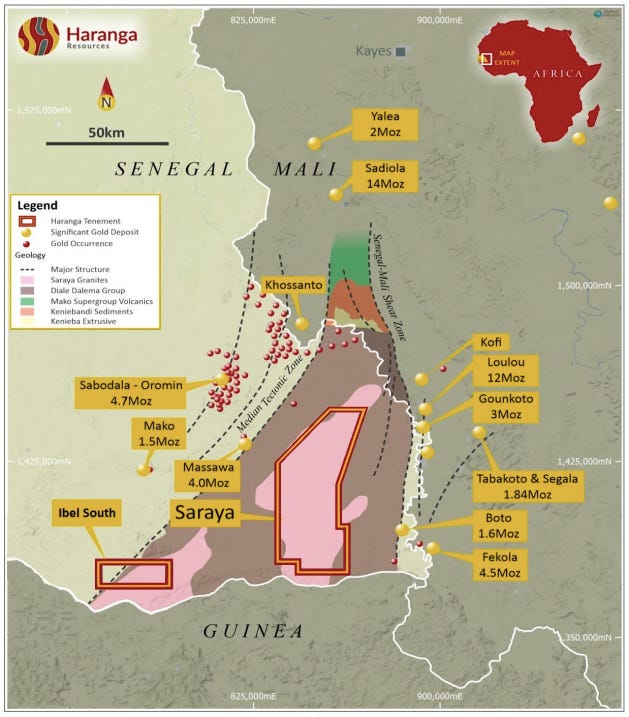

Saraya is in the mineral-rich south-eastern corner of Senegal. Obviously not a jurisdiction that screams ‘safe’, but among the best in West Africa. If you’re interested in the legal landscape for explorers and mining companies in Senegal, this guide is helpful.

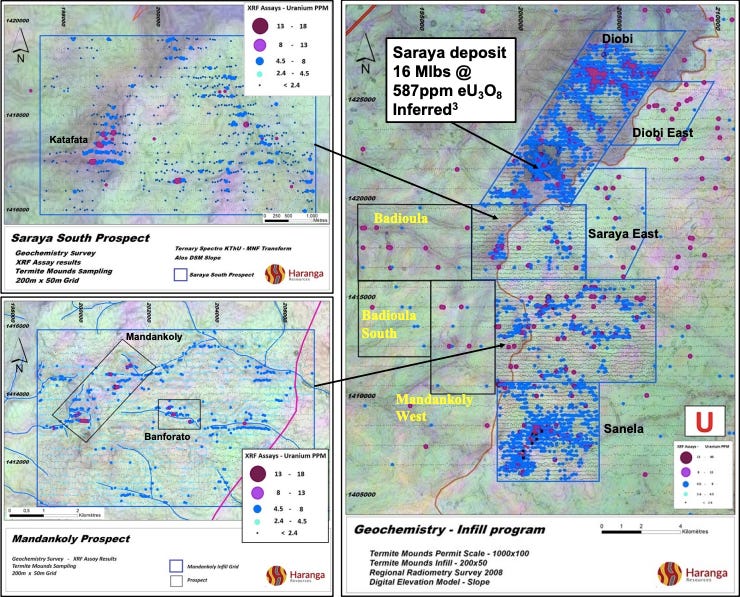

The ground had been partially explored by the French - Areva and Cogema (these entities are essentially former iterations of Orano) and the Saraya deposit - not the entire tenement - had seen substantial drilling prior to being picked up as part of the Haranga listing in 2022.

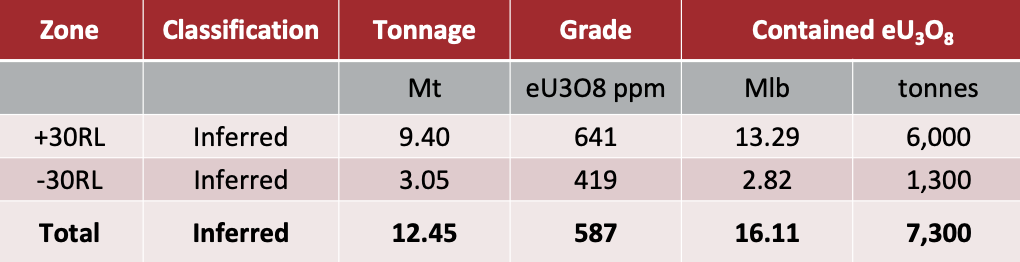

It’s hard to make out in the diagram above, but the existing resource - 16.1Mlb at 587ppm with a 250ppm cut-off - fits in a little square in towards the bottom of the green parallelogram. There’s definitely plenty of room to grow.

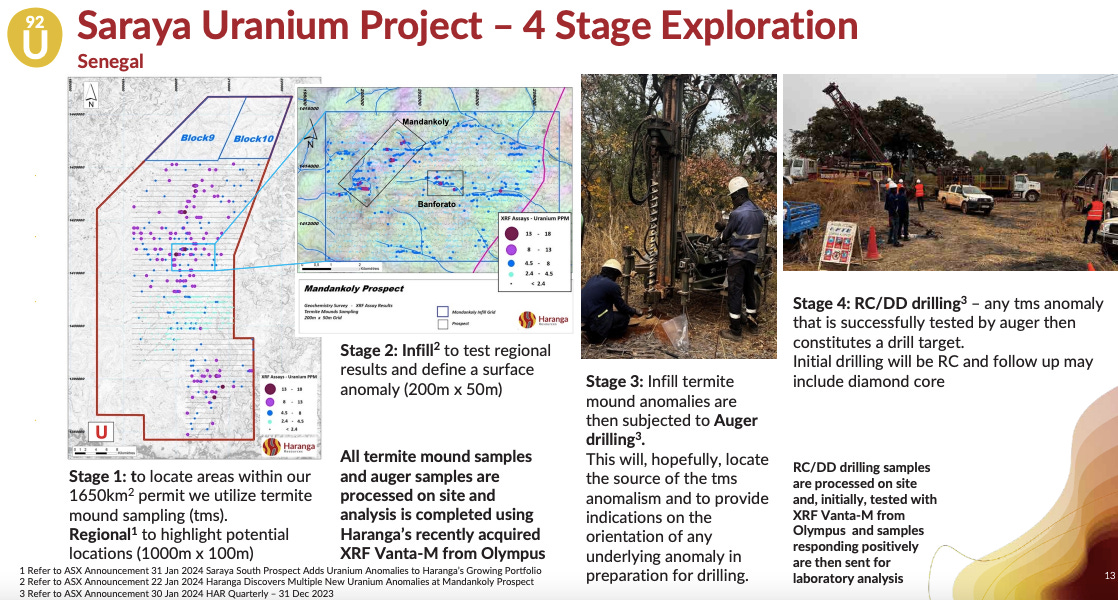

Haranga has a systematic approach to identifying new prospects across its project:

1000m x 100m termite mound sampling (TMS) to identify prospective regions

infill TMS at 200m x 50m to identify anomalies

anomalies are auger drilled to get through the lateritic hardcap and test the source

prospective targets are drilled with RC, then with a diamond core if beneficial

Across their 1650 sq km project there are already 10 prospects, some of which get better TMS indications than the Saraya deposit - it will be interesting to see what drilling turns up in Diobi, Sanela and Mandankoly.

Here is Peter Batten dodging waiters while talking about the project last month.

Ibel South Gold Project

Picked up in August 2022, “the Ibel South Gold Project lies 80km south-west of the 8.72 Moz Teranga Gold Corporation (TSX:TGZ) Sabodala-Massawa gold mine (in production) and 30km south of the 1.5Moz Resolute Mining (ASX:RSG) Mako gold mine (in production)”.

You can see the proximity to those mines in the first regional map posted earlier (just scroll back up to Saraya) but this diagram also provided insight - it shows gold anomalies with >30ppb in orange. The company should have overlaid the producing mines onto this one, but suffice to say that while the gold anomaly in the tenement makes this interesting, the lack of widespread gold anomalies over the tenement keeps it from being exciting.

That said, it’s close enough to explore from their camp at Saraya, so we’ll see if they dedicate a bit more time to it if/as the gold price continues to increase.

Where to from here?

If you believe that the uranium price is set to be strong for a few years yet, and that in that environment a company like Haranga will be able to continue funding exploration, you probably wouldn’t bet against the resource growing significantly from here. Unlike many other microcap uranium plays:

there’s already a resource

they’ve got a proven explorer running the show exploring systematically, and

there are no other political hurdles (e.g. waiting for a jurisdiction to overturn a uranium mining ban) to worry about.

Will it produce this cycle? I mean - who knows - it will be hard enough for any explorer at this early stage to get there. I imagine that if this stock turns out to be a winner, it will be through rapidly growing that resource in a positive uranium price environment, and like most African plays, it’s non-aligned, meaning that if it turns into something special, takeover offers could come from anywhere.

Could it be the next Etango (or swap in your favourite large African deposit)? They would need a lot of exploration success from here. But the grade is good for an African hard rock deposit, they’ve got plenty of territory and prospects to repeat/extend the current resource, and at $13.2m, I think the risk:reward is intriguing.

Disclaimer: This is not financial advice, and I am not a financial advisor. If you are interested in any of the ideas explored by Microcaps Anonymous, you should discuss them with your financial advisor, who will probably chastise you for looking at microcaps in the first place, and they’d probably be right!

Haven’t subscribed yet? Get free posts to your email at least once a week with deep dives into microcap stocks that might just have something to them.

Know someone who shares your passion for microcap stocks? Do them (and me!) a favour and send this post their way!