A Speculator's Guide to Sub-$50m ASX Uranium Stocks

A Speculator's Guide to Sub-$50m ASX Uranium Stocks

Brush up on all 30 companies, from smallest to largest cap!

Uranium is in a long term uptrend as the world finally gives value to nuclear’s green base load credentials, spot pounds dry up and security of supply becomes paramount. It’s cooled down in the last month or so, but the spot price is still north of $90/lb.

If you’re buying the dip, or thinking about it, you can use this as a quick reference guide for all companies:

with uranium tenements, targets or deposits,

available for purchase on the ASX,

with a market cap of less than $50m as of Sunday the 10th of March 2024.

So grab yourself a glass of something strong and let’s explore the farthest reaches of the risk curve! In true Microcaps Anonymous fashion, we’re going from smallest to largest cap.

If I’ve missed any (and these seem to be popping up all the time, so quite possible), please let me know at microcapsanonymous@gmail.com or on X.

Disclaimer: Nothing in this post is financial advice!

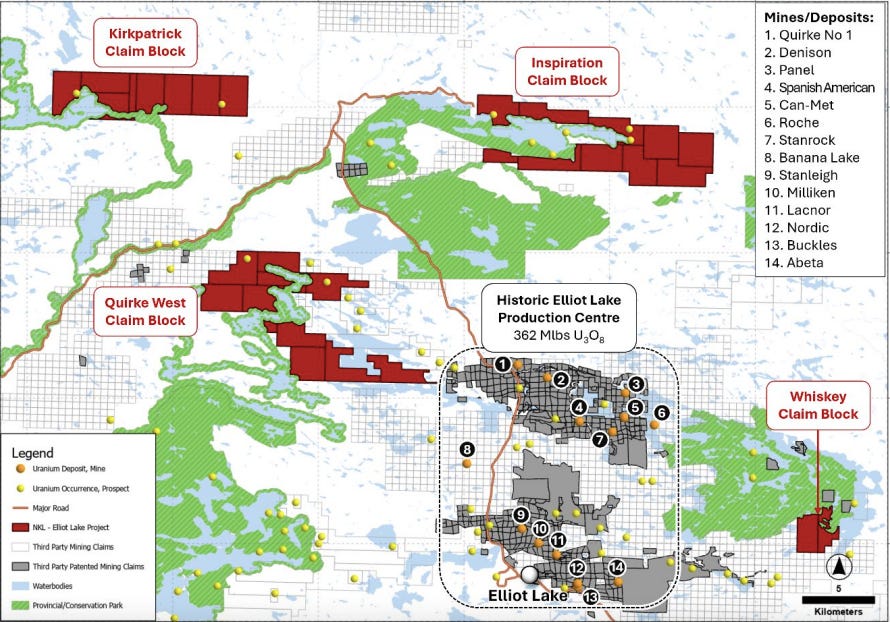

NickelX (ASX:NKL)

Project: Elliot Lake, Ontario

Market Cap: $3.2m

Cash (31/12/2023): $1.9m

That’s right. NickelX is looking for uranium. Just last month they pivoted away from, you know, nickel, and have staked ground surrounding the famed district in Ontario where 362Mlb of uranium was mined until the 1990s.

A field reconnaissance program is planned in April/May.

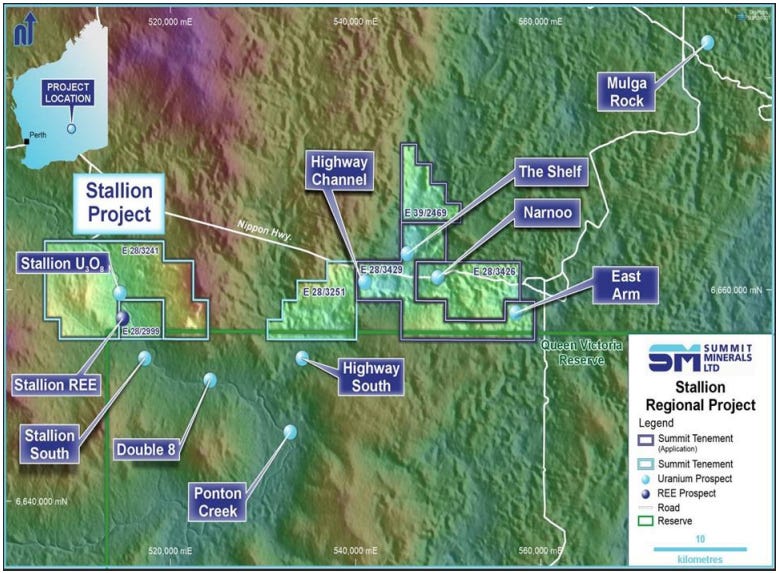

Summit Minerals (ASX:SUM)

Project: Stallion, Western Australia

Market Cap: $3.9m

Cash (31/12/2023): $2.2m

The Stallion project was orignally drilled out by Manhattan Corp (ASX:MHC) and hosts 3.3Mlb U308 at 150ppm. It lies northwest of Manhattan’s Ponton deposit and 55km from Deep Yellow’s (ASX:DYL) Mulga Rock.

They recently acquired three exploration applications which contain a further 3.7Mlb of U3O8 at 100ppm.

The State Government in WA has a 'no uranium' condition on future mining leases in place, so this will need to change if resources like this will be able to be meaningfully progressed.

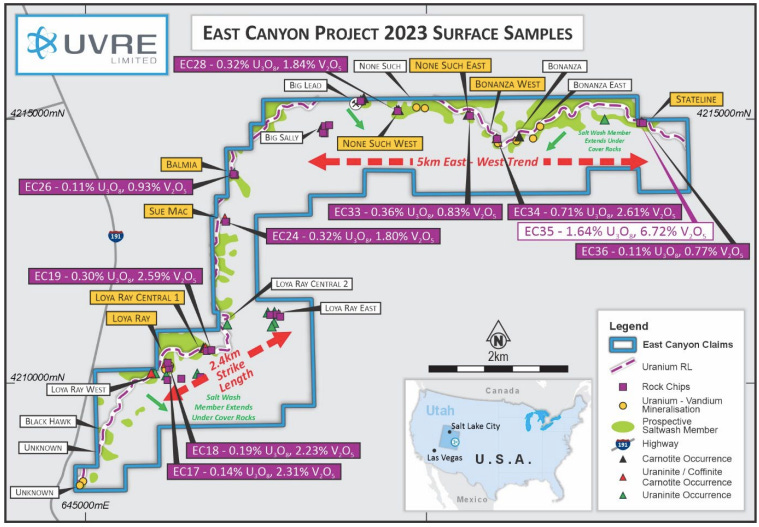

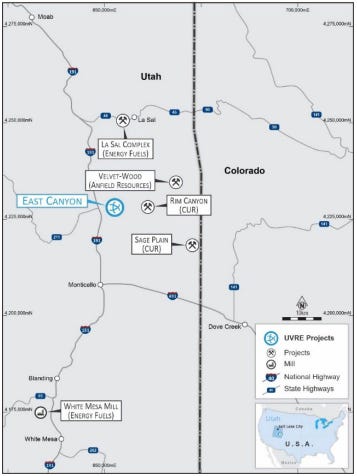

Uvre Limited (ASX:UVA)

Project: East Canyon Project, Utah

Market Cap: $4.5m

Cash (31/12/2023): $2.9m

Located between Energy Fuels’ (NYSE:UUUU) White Mesa Mill and its La Sal complex, Uvre has done limited exploration of its project area in Utah since listing in June 2022. Rock chip samples recently returned up to 1.64% U3O8.

The company has a similarly early stage lithium project in Wyoming.

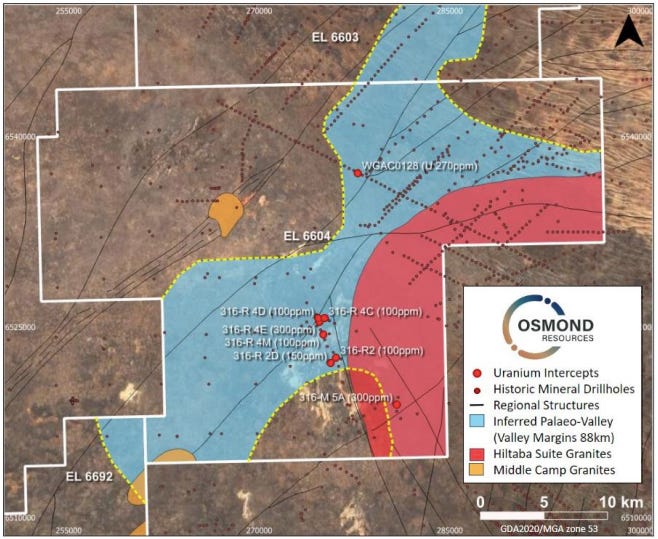

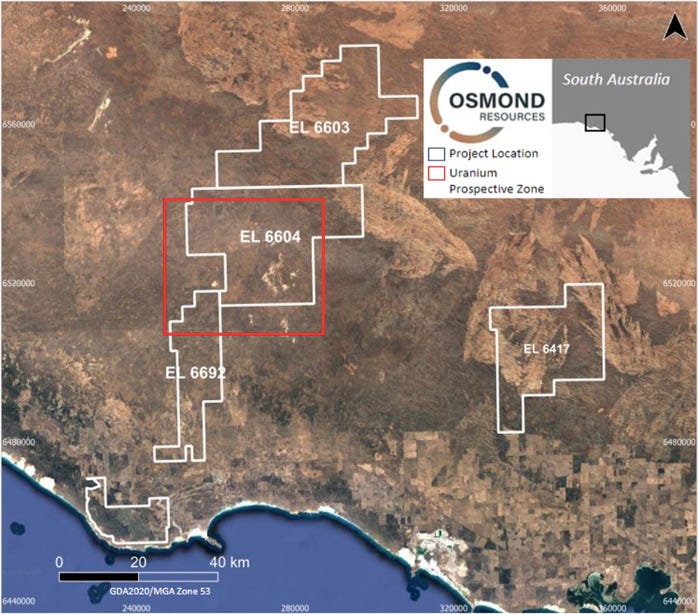

Osmond Resources (ASX:OSM)

Project: Fowler, South Australia

Market Cap: $4.8m

Cash (31/12/2023): $4.6m

Trading at close to cash value, Osmond Resources has recently reported uranium potential at their South Australian Fowler project, with “potential uranium roll-front system hosted in sands and clays within 10 to 30m of the surface and over a large strike length, up to 20km”. Exploration programs are currently being defined.

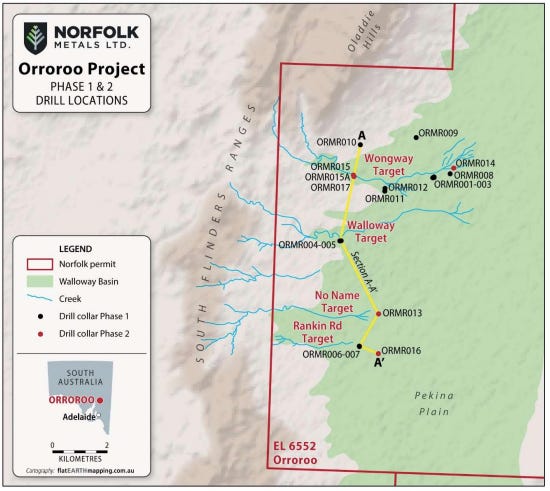

Norfolk Metals (ASX:NFL)

Project: Orroroo, South Australia

Market Cap: $5m

Cash (31/12/2023): $3.5m

Norfolk Metals recently completed a 17-hole drill program - their first at Orroroo - intersecting a uranium-bearing floodplain. From that release:

“Overall, the drilling results suggests that the primary target model remains to be a Beverley deposit type uranium model where the highest grades of uranium are expected to be located at the base of the incising part of the palaeochannel with lower uranium grades seen in the floodplains. It is the intent of the company to continue the exploration efforts around the Wongway Creek Target by defining the uranium bearing palaeochannel through either/both geophysics and close-spaced drilling.”

The company also have an early stage copper-gold exploration project in northwest Tasmania. They listed in March 2022.

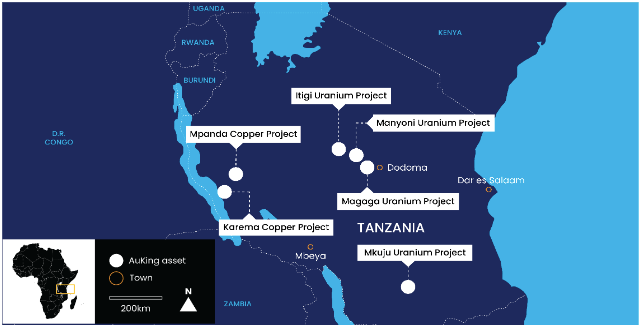

Auking Mining (ASX:AKN)

Project: Mkuju, Mayoni & Magaga, Tanzania

Market Cap: $5.1m

Cash (31/12/2023): $400k

Auking’s Mkuju project borders the 125Mlb Nyota deposit, discovered by Mantra Resources during the last cycle, leading to their takeover in 2011 for $1.02b by Russia’s Rosatom. An 11,000m drilling campaign will commence in May, at the conclusion of the wet season.

The Mayoni project is the subject of an ongoing dispute with the Tanzanian Mining Commission, after two of the five Prospecting Licences covering the project - those which contained the majority of a historical resource (92Mt at 100ppm cutoff with 29Mlb contained U3O8) - were revoked and granted to another party only a week after they were granted to Auking in Febraury 2023.

Last year, the company also completed a Scoping Study over its copper-zinc project in the Halls Creek region of Western Australia.

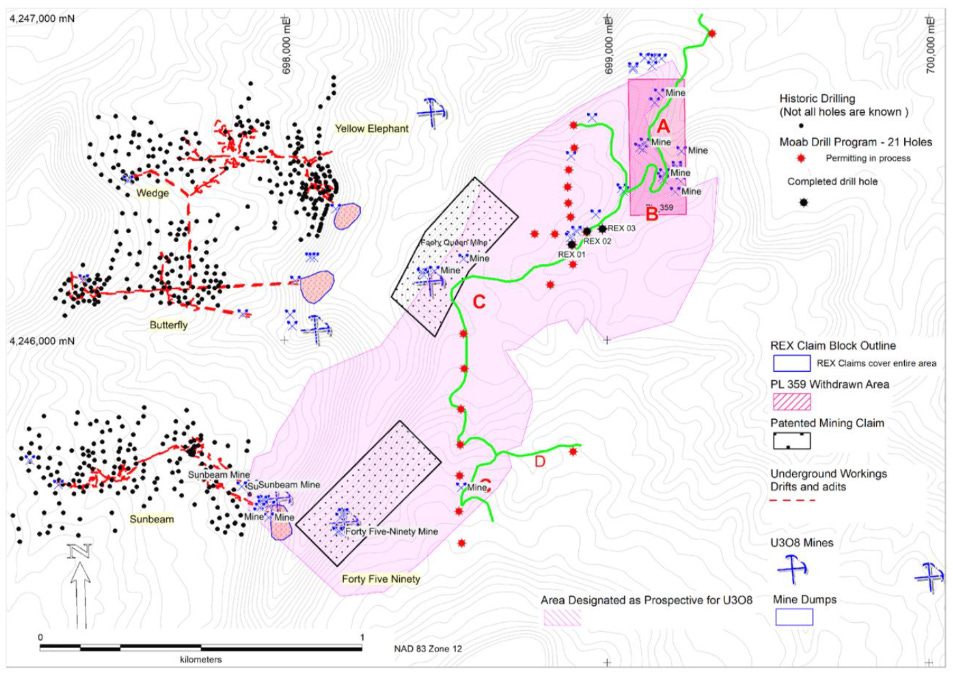

Moab Minerals (ASX:MOM)

Project: REX Uranium-Vanadium Project, Colorado (60% owned)

Market Cap: $5.1m

Cash (31/12/2023): $2.8m

Moab owns 60% of the REX U-V Project in the Uravan Mineral Belt in Colorado.

Drilling results from October 2023 showed uranium mineralisation in REX01 only (below) - further drilling (red) is planned to test eastern extensions of historical mines.

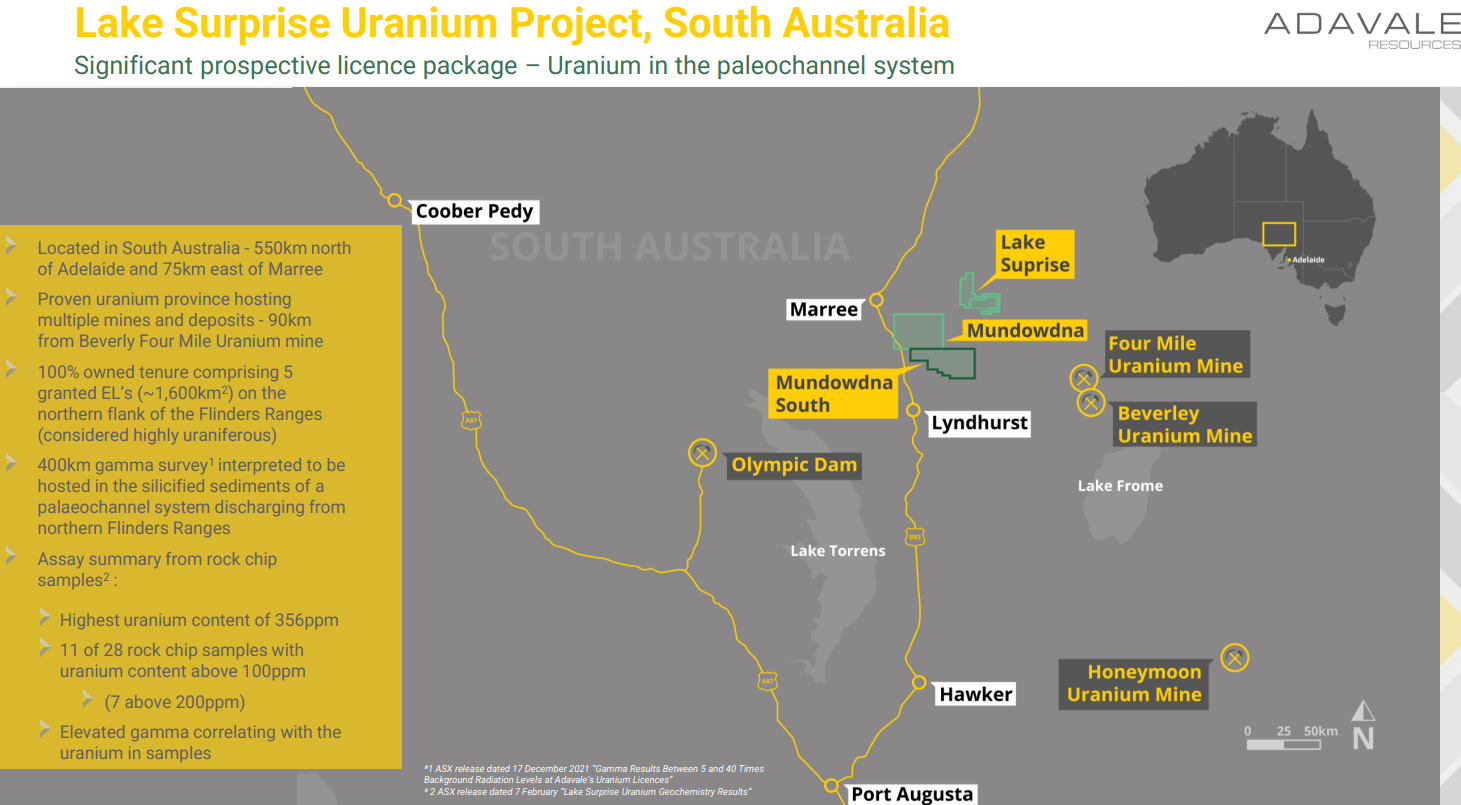

Adavale Resources (ASX:ADD)

Project: Lake Surprise, South Australia

Market Cap: $5.1m

Cash (31/12/2023): $2.5m (includes $1.5m raised in January 2024)

Adavale Resources’ Lake Surprise project lies 90km west of the Four Mile and Beverley Uranium mine. After reconnaissance drilling at Lake Surprise early last year suggested potential to the south, the Mundownda South tenement was picked up in September, and this is where exploration will be focussed in 2024.

Their second project - their priority until recently - is the Kabanga Jirani nickel project in Tanzania. It is adjacent to and along strike from the world’s largest ‘under development’ high-grade Kabanga nickel sulphide deposit, which is owned by BHP-backed Lifezone Metals.

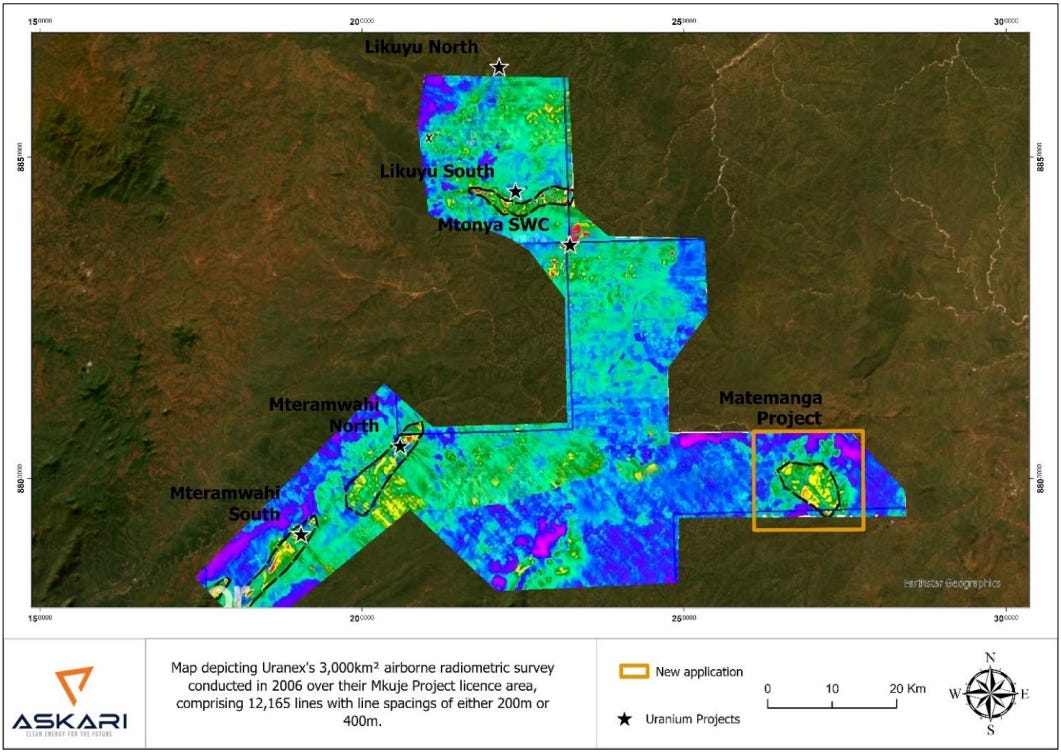

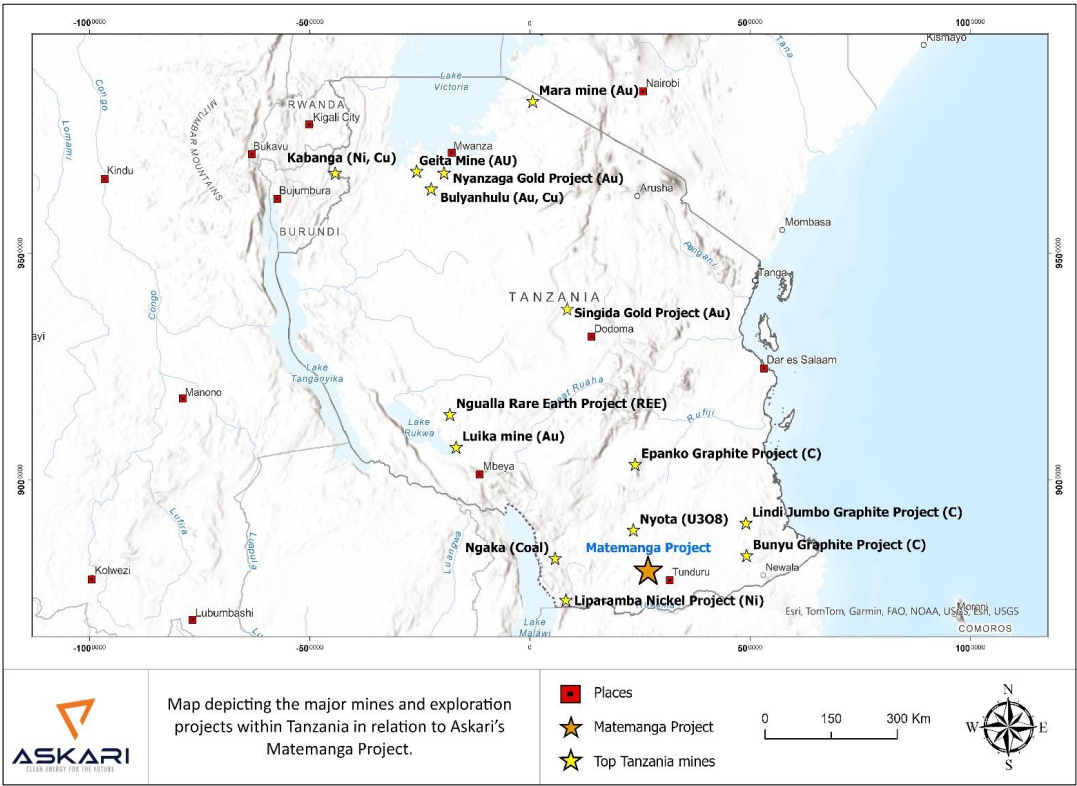

Askari Metals (ASX:AS2)

Project: Matemanga, Tanzania

Market Cap: $6.8m

Cash (31/12/2023): $700k

Since listing in July 2022, Askari had been targeting lithium in Namibia at its flagship Uis project. Just last month, however, they picked up the Matemanga project in southern Tanzania, staking a radiometric anomaly that was identified, but not followed up, when discovered in 2006.

Manhattan Corporation (ASX:MHC)

Project: Ponton, Western Australia

Market Cap: $7.3m

Cash (31/12/2023): $2.7m

The 17.2Mlb (at 300ppm) Ponton deposit is located 40km from Deep Yellow’s (ASX:DYL) Mulga Rock. Unlike Mulga Rock, which has an exemption, any future mining lease would have a ‘no uranium’ condition. There is currently an effort to have this regulation relaxed (pushed very publicly by Cauldron Energy (ASX:CXU) CEO Jonathon Fisher), and so MHC plan to request Ministerial Consent to explore the deposit and surrounds further.

Fun fact: the company did 17x from COVID lows (0.3c) to September 2020 highs (5.2c) off the back of results from their Tibooburra Gold Project in NSW, which they still hold, but have since come full circle and traded again as low as 0.2c this month.

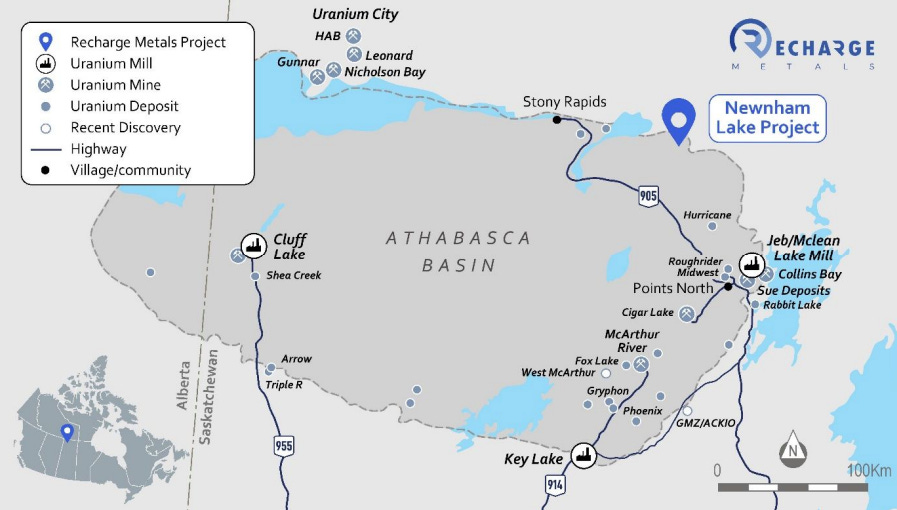

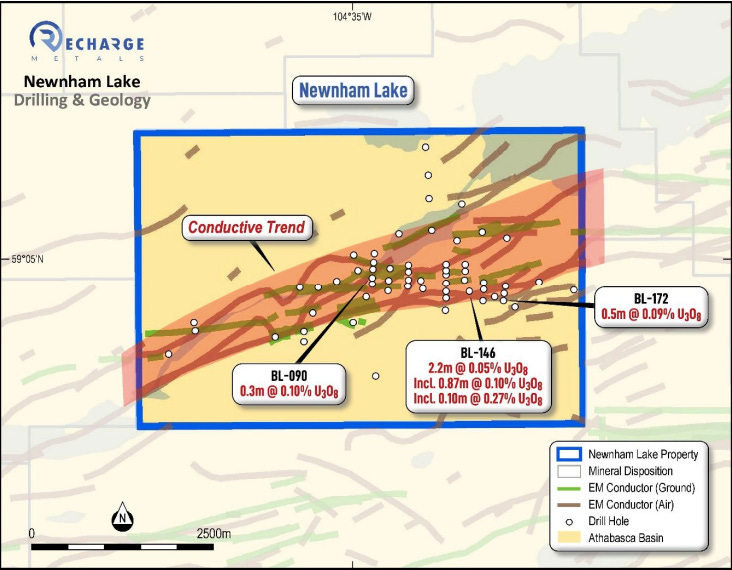

Recharge Metals (ASX:REC)

Project: Newnham Lake, Saskatchewan

Market Cap: $8.8m

Cash (31/12/2023): $1.3m

Until this month, a lithium explorer in Canada. Now, with a 15 sq km block 56km northwest of IsoEnergy Ltd’s (TSX.V: ISO) 48.6Mlbs at 34.5% Hurricane Deposit, at the northeastern tip of the Athabasca basin, the plan is to drill test the basement rock.

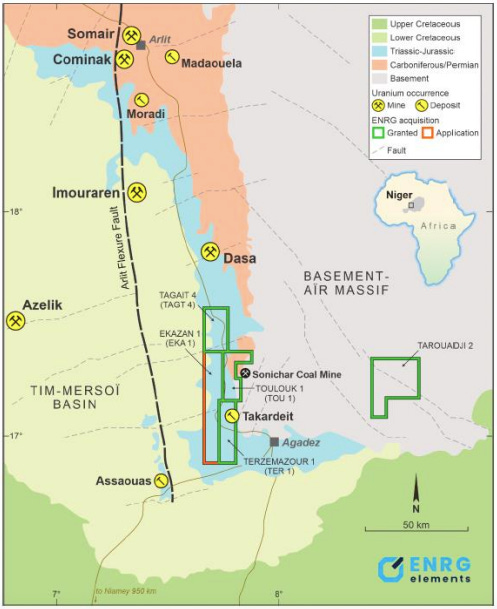

ENRG Elements (ASX:EEL)

Project: Agadez, Niger

Market Cap: $9.1m

Cash (31/12/2023): $1.3m

Around 50km south of Global Atomic’s (TSX:GLO) Dasa development project, due to come online in Q4 2025, ENRG Elements suffered greatly in the political turmoil which kicked off in July 2023, with their share price dropping to 0.3c in early August. Despite the situation seemingly having calmed since then, the stock is at 0.8c, having seen a high of 5.4c in 2022.

The company has a resource of 21.5Mlb U3O8 at 315ppm (175ppm cutoff) and are back on the ground after a disrupted H2 2023. A trenching program is currently taking place.

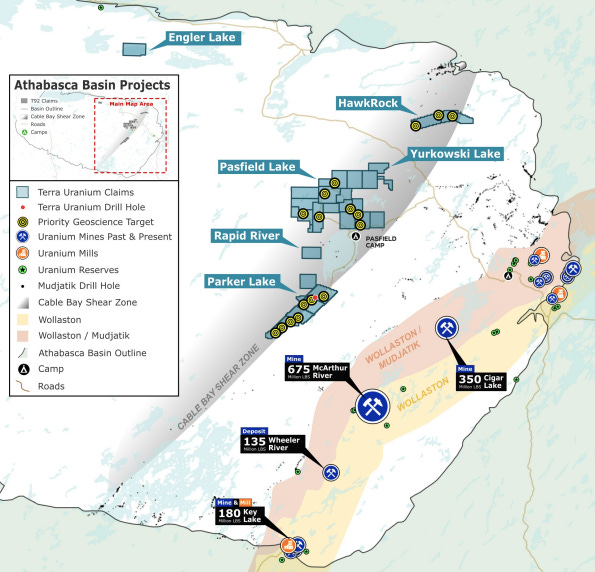

Terra Uranium (ASX:T92)

Project: Pasfield Lake, Parker Lake, HawkRock, Engler Lake, Rapid River & Yurkowski Lake, Saskatchewan

Market Cap: $10.7m

Cash (31/12/2023): $800k

Terra Uranium is led by Andrew Vigar (co-founder of Alligator Energy (ASX:AGE) and has Doug Engdahl on the board - current MD of Atha Energy (TSXV:SASK), which is currently finalising its acquisition of 92 Energy (ASX:92E).

Looking deeper in the Athabasca Basin - along the Cable Bay Shear Zone - their ~1000m deep holes are expensive to drill, and T92 is looking for partners to fund drilling this spring/summer.

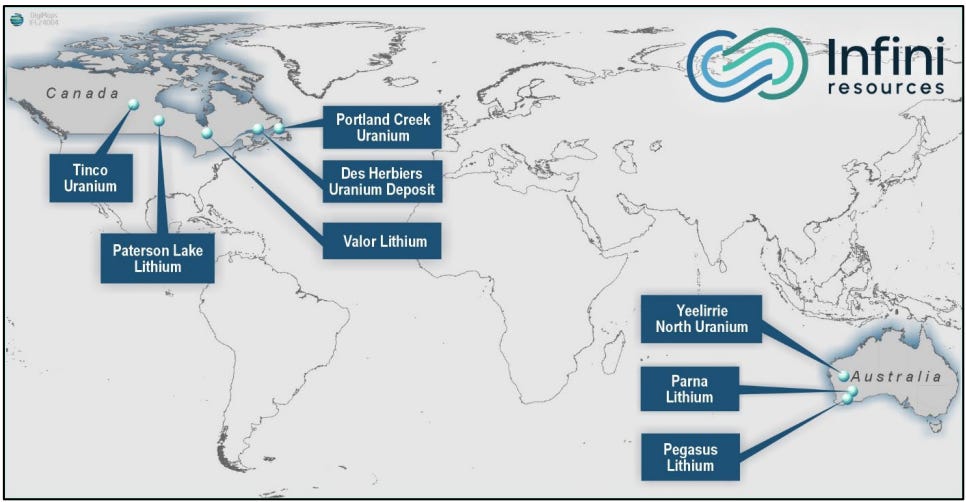

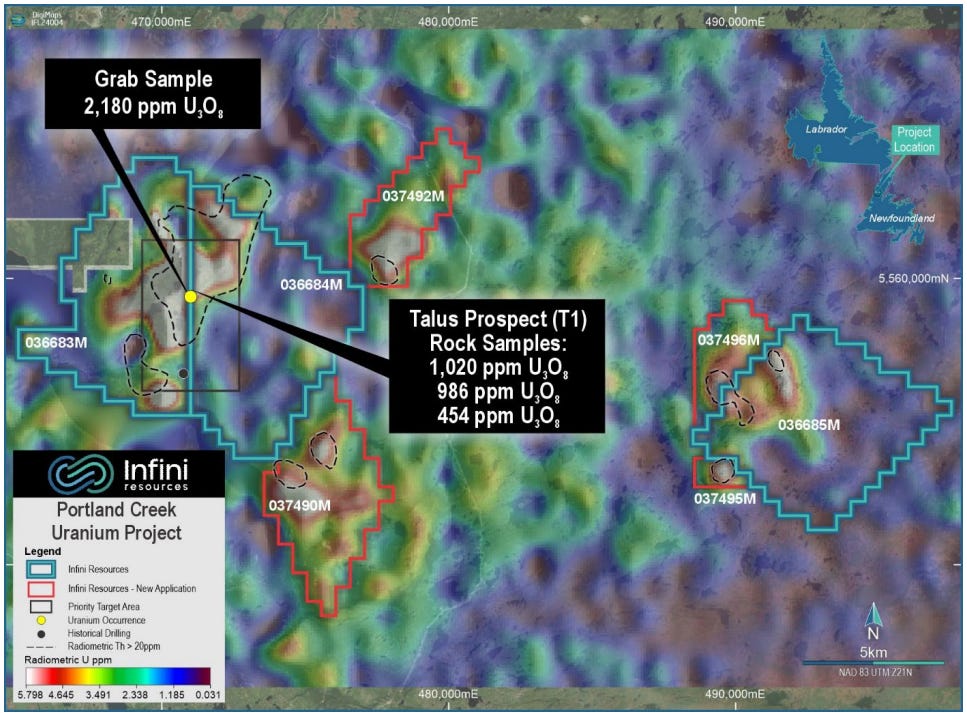

Infini Resources (ASX:I88)

Projects: Canada - Portland Creek, Newfoundland; Paterson Lake, Ontario; Des Herbiers Deposit, Quebec; Tinco, Saskatchewan (50%). Australia - Yeelirrie North, Western Australia.

Market Cap: $11.3m

Cash (15/1/2024): $5.3m raised at IPO - listed January 2024

Recently listed Infini has a range of projects targeting uranium and lithium.

Initial work has been focussed on the Portland Creek Uranium Project in Newfoundland, where drilling has never been conducted.

Two of their projects depend on changes to legislation. The first is the 44Mlb at 123ppm Des Herbiers deposit in Quebec, where a moratorium on uranium mining and exploration is currently in place. The second is the Yeelirrie North project in Western Australia, where the state government will not grant uranium mining leases.

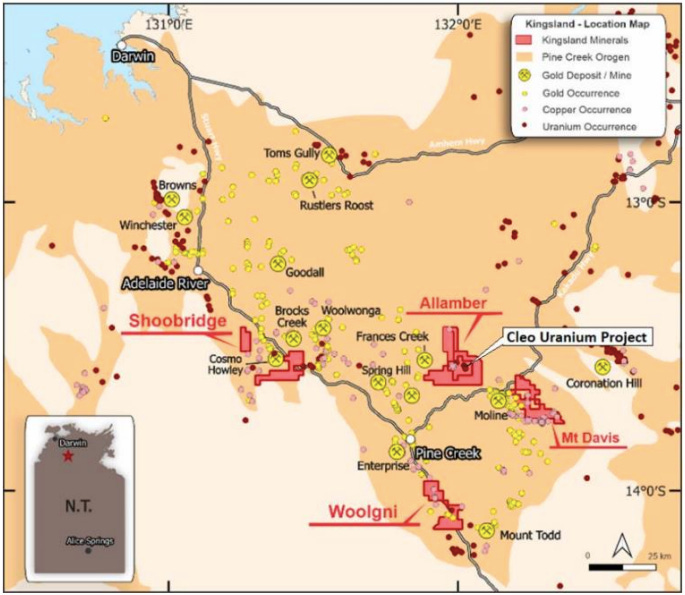

Kingsland Minerals (ASX:KNG)

Project: Cleo, Northern Territory

Market Cap: $12.5m

Cash (31/12/2023): $2.4m

After listing in 2022 with the Cleo deposit as the company’s flagship asset, Kingsland is now focusing on its “potentially world-class Leliyn Graphite Project in the Northern Territory”.

So while the project, with its 5.2Mlbs U308 at 345ppm is likely to go elsewhere, it will be interesting to see where it ends up.

Valor Resources (ASX:VAL)

Project: Cluff Lake, Surprise Creek, Hidden Bay, Hook Lake & Beatty River, Saskatchewan

Market Cap: $13.7m

Cash (31/12/2023): $2m

While no drilling has been completed since 2022, when the company ran an 8-hole program at Hook Lake, Valor has put together a set of Athabasca Basin projects in the last few years. Q2 2024 is dedicated to planning drilling at Hidden Bay and Cluff Lake.

The company also has Peruvian copper assets (JV with Firetail Resources ASX:FTL) and has acquired lithium tenements in Ontario.

Koba Resources (ASX:KOB)

Project: Yarramba, South Australia

Market Cap: $14.3m

Cash (31/12/2023): $4.2m

Koba Resources was spun out of copper explorer New World Resources (ASX:NWC) in 2022. Going after cobalt and lithium since then, in January it purchased 80% the Yarramba project from Havilah Resources (ASX:HAV), which borders the northern edge of Boss Energy’s Honeymoon project and is in the same paleochannel system. They’ve since picked up two 100% owned tenements to the north.

The Oban Uranium Deposit is on the 80% owned tenements, and a JORC 2004 resource estimate (note, JORC 2012 is now the minimum standard for reporting) gave it 4.6Mlb U308 at 260ppm. Drilling is expected to commence in Q2 2024.

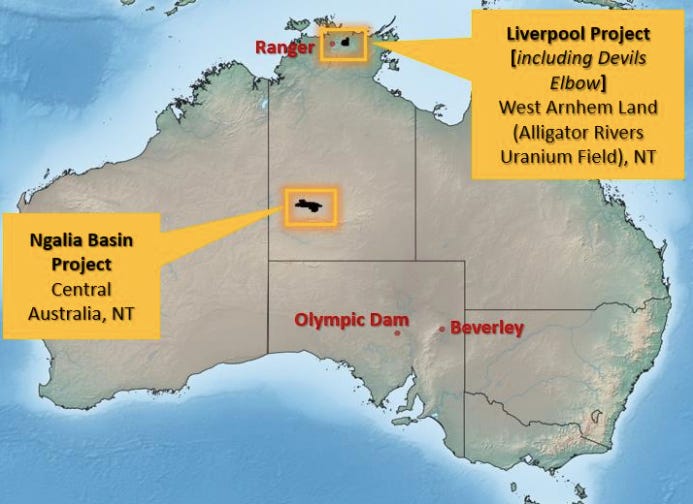

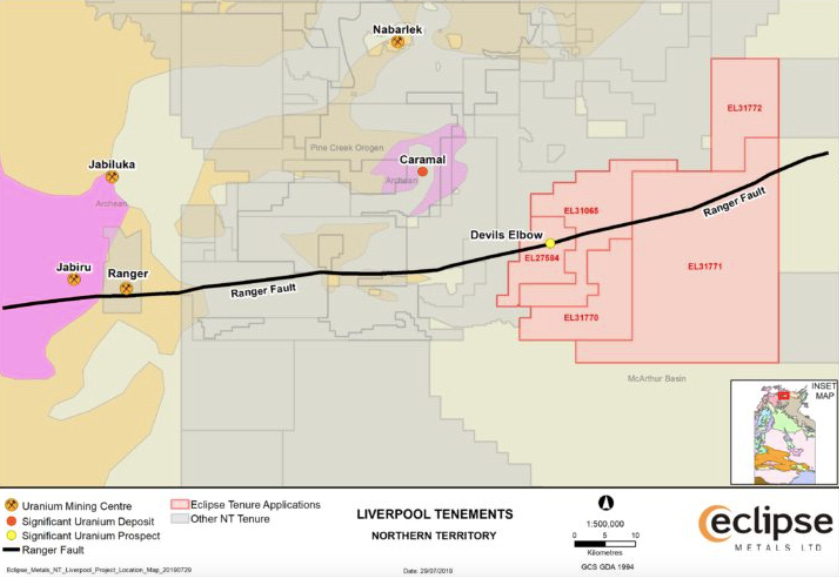

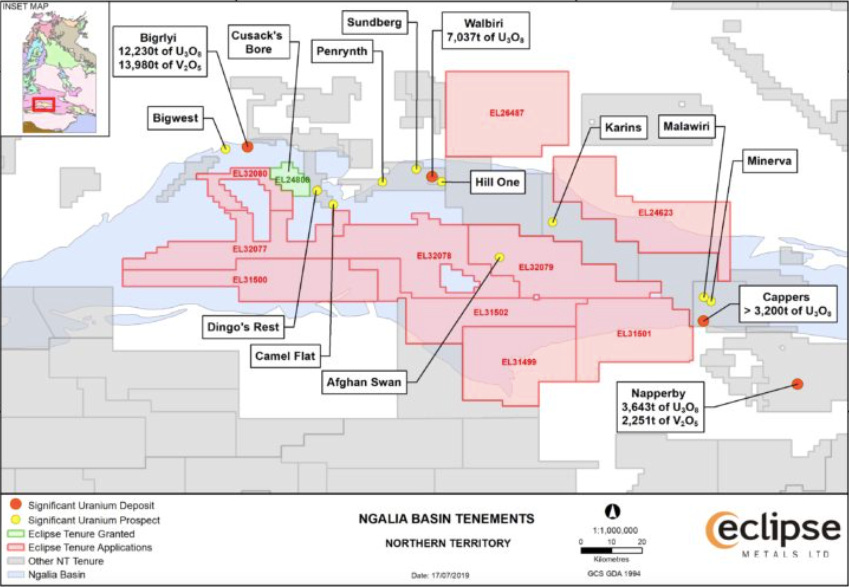

Eclipse Metals (ASX:EPM)

Project: Liverpool & Ngalia Basin, Northern Territory

Market Cap: $14.5m

Cash (31/12/2023): $900k

Eclipses is focused on advancing its a rare earth elements (REE) project in Greenland, and is currently planning to spin out its Liverpool and Ngalia Basin Projects, comprising 6,211 sq km of ground across 13 tenements in the Northern Territory, and list them on the ASX as ‘Oz Yellow’.

The Ranger Fault cuts through the Liverpool Project, which is in the same Alligator Rivers region that is host to Jabiluka, Ranger and Nabarlek.

The Ngalia Basin hosts several deposits, the most notable being Energy Metals’ (ASX:EME) Bigrlyi at 21Mlb at 1283ppm U3O8.

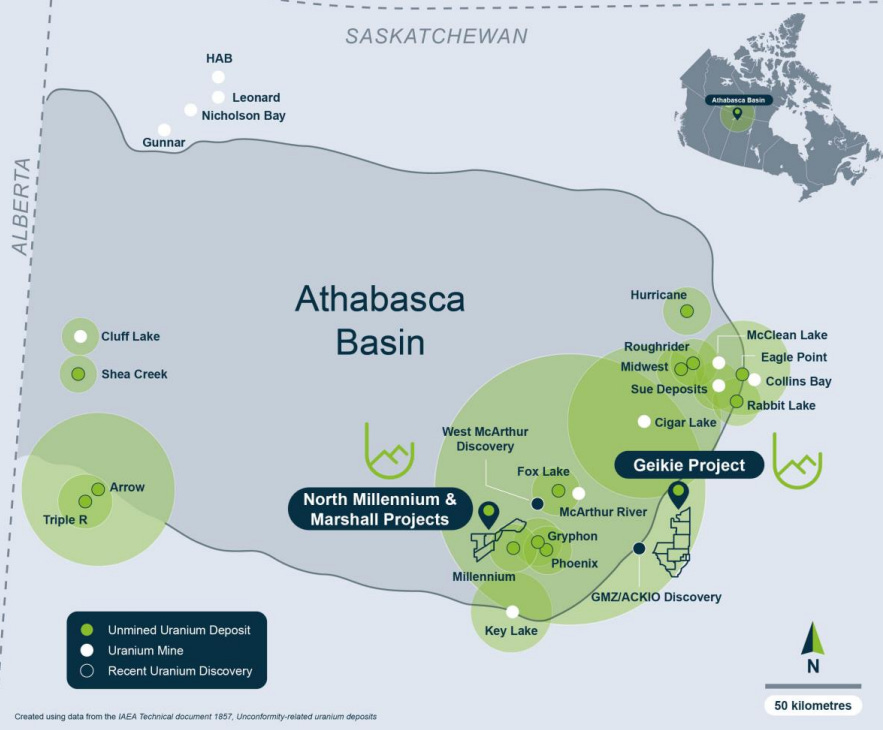

Basin Energy (ASX:BSN)

Project: North Millennium, Marshall & Geikie, Saskatchewan

Market Cap: $14.6m

Cash (31/12/2023): $7.7m (includes $3.3m raised in February 2024)

With assets in and around the Athabasca basin, Basin Energy is on-site to commence drilling at the Geikie project, and plans to drill at the North Millennium project in Q2 2024.

The North Millennium and Marshall projects are located in the southeastern portion of the Athabasca Basin and situated 7km north of Cameco’s Millennium uranium deposit, host to 104.8Mlb U3O8 at 3.76%.

Haranga Resources (ASX:HAR)

Project: Saraya, Senegal

Market Cap: $15.2m

Cash (31/12/2023): $2m

Termites do the hard work of bringing uranium and pathfinders to surface, and Haranga’s ongoing four-stage exploration process is taking good advantage of their labour. In ongoing exploration, termite mound sampling (TMS) suggests auger drilling targets, which in turn identify RC drilling targets.

The company has an inferred resource of 16.1Mlbs at 587ppm (250ppm cutoff) at Saraya announced last September, and are helmed by Managing Director Peter Batten, who originally delineated Bannerman Energy’s (ASX:BMN) Etango project in the last cycle.

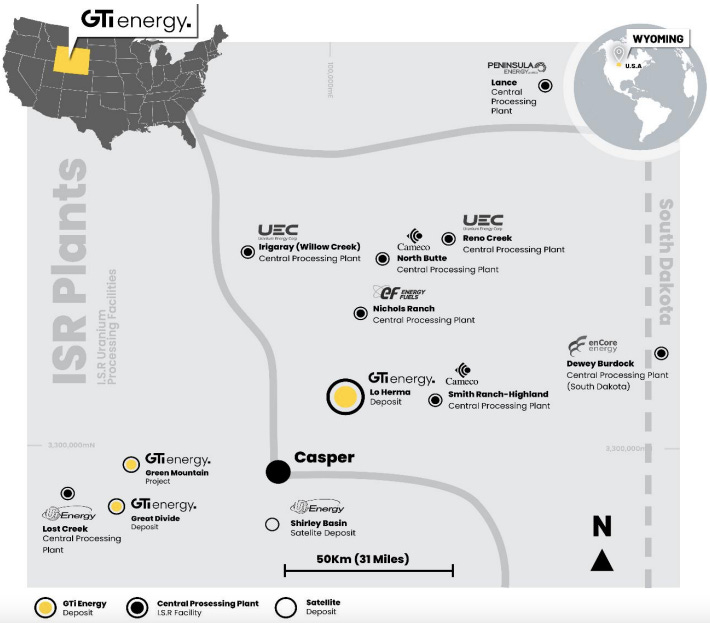

GTI Energy (ASX:GTR)

Projects: Lo Herma, Great Divide Basin & Green Mountain, Wyoming; Henry Mountains, Utah

Market Cap: $17.4m

Cash (31/12/2023): $2.1m

GTI has various projects in Wyoming that are amenable to ISR, situated among various well-known North American uranium names. The Lo Herma and Great Divide Basin projects have a combined inferred Mineral Resource Estimate of 7.37Mlb U3O8 at around 600ppm.

The company intends to drill Lo Herma in Q3 2024 & update the resource estimate in Q4.

Orpheus Uranium (ASX:ORP)

Projects: South Australia - Frome, Woolshed, Mundaerno, Radium Hill South, Marree, Cummins; Northern Territory - Ranger North-East, Woolner, T-Bone, Mt Douglas

Market Cap: $17.8m

Cash (31/12/2023): $5.3m

Formerly Argonaut Resources (until last month), Orpheus Uranium has acquired various tenements in South Australia, some targeting the same paleochannels that host Honeymoon, Beverley and Four Mile, as well as several in the Northern Territory.

Exploration is at an early stage.

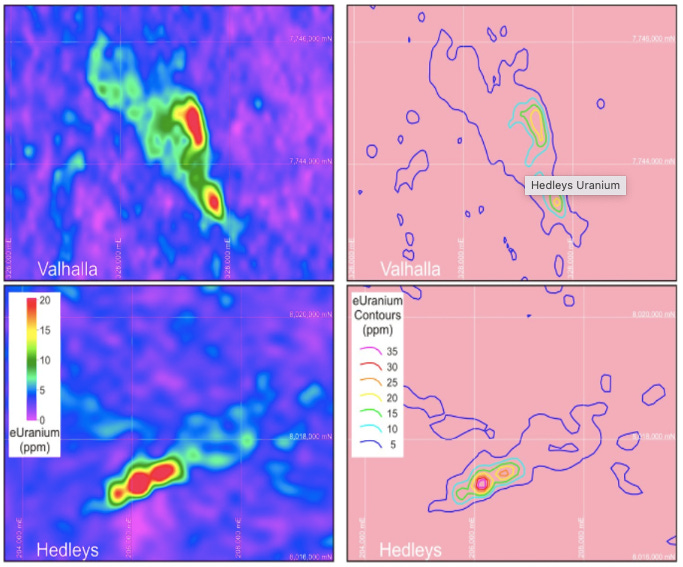

Superior Resources (ASX:SPQ)

Project: Hedleys, Queensland

Market Cap: $22m

Cash (31/12/2023): $2.1m

Disclaimer - this one is a stretch. Superior Resources spends most of its time looking for porphyry copper (and various other metals) in northern Queensland. Their tenure hosts the Hedleys uranium prospect, but while the state forbids uranium mining, it’s hard to see much happening on that front.

As a “strong localised airborne uranium radiometric anomaly associated with a major fault”, the company sees potential for it to be analogous to Paladin’s (ASX:PDN) nearby Valhalla deposit.

Gladiator Resources (ASX:GLA)

Project: South West Corner, Minjingu, Liwale, Mkuju, Foxy & Eland, Tanzania

Market Cap: $22m

Cash (31/12/2023): $4.2m (includes $4m raised in March 2024)

Gladiator reported their highest grade results to date with grades of up to 7139ppm (~0.7%) recorded in trenching assays at their South West Corner (SWC) prospect, which is hosted in the same rock type as Uranium One/Rosatom’s Nyota deposit 50km to the north (124.6Mlbs U3O8 at 306ppm).

They recently raised $4m to expedite exploration across their projects.

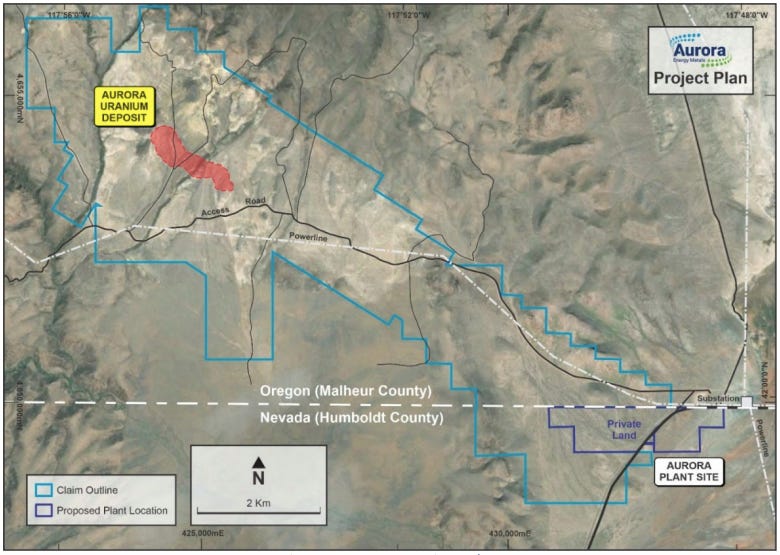

Aurora Energy Metals (ASX:1AE)

Project: Aurora Energy Metals Project, Oregon/Nevada

Market Cap: $22.3m

Cash (31/12/2023): $2.6m

Aurora has a uranium deposit in Oregon, and land on which it could potentially build a processing plant just across the border in Nevada. The deposit contains 50.6 Mlb U3O8 at 214 ppm, but a Scoping Study is currently being undertaken on the shallow high-grade core, which has 19.2 Mlb U3O8 at 485 ppm of which 90% is Measured.

The Scoping Study is due to be complete by the end of Q1.

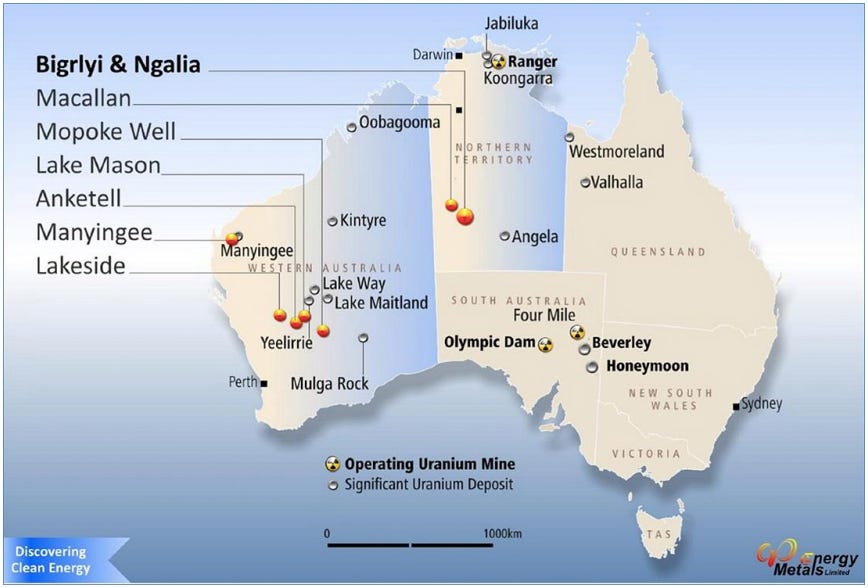

Energy Metals (ASX:EME)

Project: Northern Territory - Bigrlyi, Ngalia & Macallan, Western Australia - Mopoke Well, Lake Mason, Anketell, Manyingee & Lakeside

Market Cap: $26.2m

Cash (31/12/2023): $13.2m

Energy Metals is 66.45% owned by a subsidiary of Chinese state-owned energy corporation China General Nuclear Power Group, CGN. They have various projects and joint ventures in the Northern Territory and Western Australia.

There are several separate small resources (less than 3-5Mlb), but the only one on note is Bigrlyi, which has 21Mlb at 1283ppm (500ppm cut-off). This was estimated in 2011, and a MRE update to JORC 2012 standard is due this month.

Global Uranium and Enrichment (ASX:GUE)

Project: Colorado - Tallahassee & Maybell, Saskatchewan - Athabasca Basin (various), Utah - Rattler

Market Cap: $29m

Cash (31/12/2023): $6.5m (includes $6.15m raised in February 2024)

The flagship asset of GUE, formerly Okapi Resources, is the Tallahassee project in Colorado, which hosts 49.8Mlb U308 at 540ppm (250ppm cut-off). The company has various other North American exploration assets.

They recently completed a $6.15m raise to fund drilling at the Tallahassee and Maybell Uranium Projects in the U.S. and are targeting the release of a Scoping Study for the Tallahassee project in H2 2024.

West Wits Mining (ASX:WWI)

Project: Bird Reef, South Africa

Market Cap: $43.7m

Cash (31/12/2023): $1.4m ($74.1m financing available for gold project development)

West Wits is a soon-to-be gold miner in the historically prolific Witswatersrand Basin, where historically 1.5 billion (with a ‘b’) ounces of gold have been produced. Uranium is included as part of the company’s miner’s right, and it has an exploration target of 12 to 16Mlb U308 at 300-550ppm.

A three-hole diamond drilling program occurred at Bird Reef in 2022, the best result achieving 1.59m at 835ppm. Two follow-up programs are planned, 10 holes at 2640m and 2 holes at 1600m.

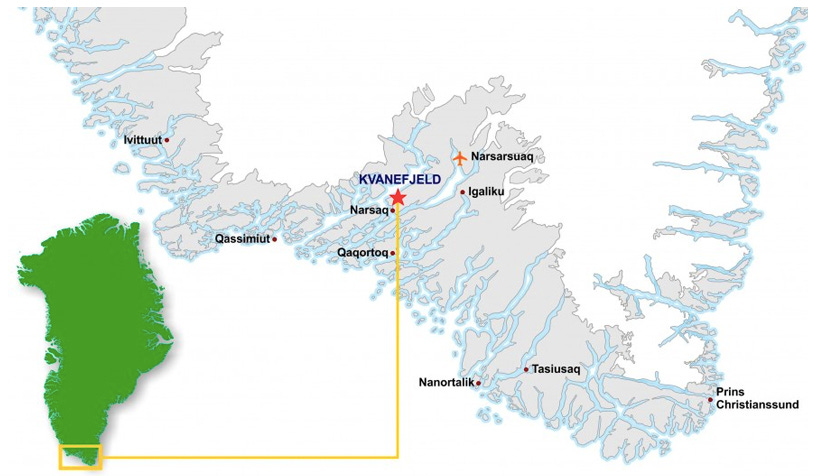

Energy Transition Minerals (ASX:ETM)

Project: Kvanefjeld, Greenland

Market Cap: $ 47.6m

Cash (31/12/2023): $16.1m

Energy Transition Minerals used to be called Greenland Minerals. Kvanefjeld is a world-class rare earths and uranium deposit in Greenland with an enormous mineral endowment, including over 368Mlb U3O8 at 248ppm (150ppm cut-off(.

So what is it doing here with this lowly valuation? In December 2021, legislation was passed in Greenland that stopped Greenland Minerals from from turning their exploration licence into an exploitation licence. This was after $130m had been invested in exploration over 10 years.

Arbitration commenced early in 2022 and is ongoing.

In a recent strategic update, the company has said while it fights to reclaim value for its Greenland asset, it will embark on low-cost exploration on its lithium projects in Spain and Quebec, while potentially examining other battery/energy projects in Tier 1 jurisdictions.

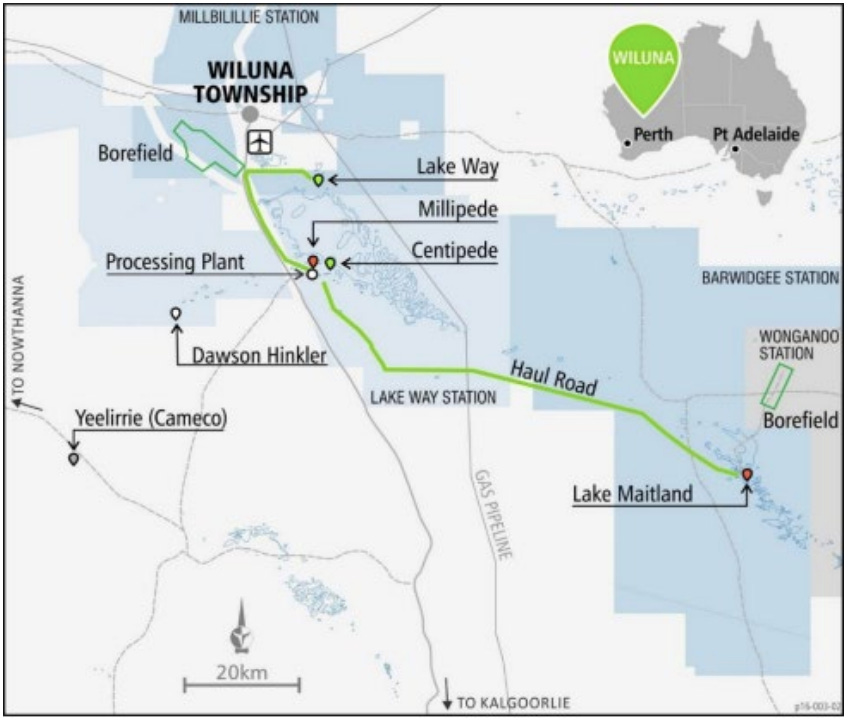

Toro Energy (ASX:TOE)

Project: Wiluna, Western Australia

Market Cap: $48.1m

Cash (31/1/2024): $15.1m

The Wiluna project was one of four projects that did not fall under Western Australia’s uranium mining ban in 2016 as it had already received Stage Government approval (of the other three, two belong to Cameco - one being Yeelirrie in the image below - and the other is Deep Yellow’s Mulga Rock).

A Scoping Study for a uranium-vanadium mine was completed in October 2022, which had a pre-tax NPV8 of $610m (post-tax wasn’t published…) over a 17.5 year mine life, with 1.3Mlb of uranium and 0.7Mlb of vanadium per year. The price of uranium has risen significantly since then, and the company has started publishing new resource estimates with lower cutoffs to reflect this.