Southern Palladium (ASX:SPD)

Southern Palladium (ASX:SPD)

Impressive South African PGM stock that nobody is talking about is hiding in plain sight

It’s been a real challenge to figure out how to get into this article for you, so I’m stripping it right back:

Successful speculators say to buy capitulation and sell euphoria.

Commodity prices have cycles, and capitulation occurs towards the bottom.

Based on commodity prices, PGM stock prices and market sentiment, platinum group metals (PGMs) seem to be much closer to cycle lows than cycle highs.

Supply of PGMs is highly concentrated (>90%) in South Africa, Russia and Zimbabwe, where most economically viable resources are.

For country-specific reasons (electricity and social unrest in South Africa, sanctions in Russia, Zimbabwe in Zimbabwe), this supply is at risk of downside shocks.

Automotive demand is the primary driver of PGM demand at the margin: ICEs, Hybrid EVs and Fuel Cell EVs (FCEVs) require PGMs for catalytic converters, but they play a much reduced role in pure battery EVs.

If PGMs are at risk of supply shocks, and the demand story may be helped by a slower than anticipated death of the internal combustion engine (or equally by a faster than hoped uptake in FCEVs), there’s a half decent chance of higher PGM prices over the coming 3-5 years, in either a spike or a fundamentally driven scenario.

A well managed, lowest quartile in the cost curve, PGM-focussed microcap which is a stone’s throw from world class global players and their infrastructure would likely do well in this scenario.

Today you’ll learn about an ASX-listed microcap whose project is nestled between the big South African players in the enormously prolific Bushveld Complex.

Disclaimer: This is not financial advice, and I am not a financial advisor.

Contents

Chart

Financials

Project

People

Where to from here?

Haven’t subscribed yet? Get free posts to your email at least once a week with deep dives into microcap stocks that might just have something to them.

Know someone who shares your passion for microcap stocks? Do them (and me!) a favour and send this post their way!

Chart

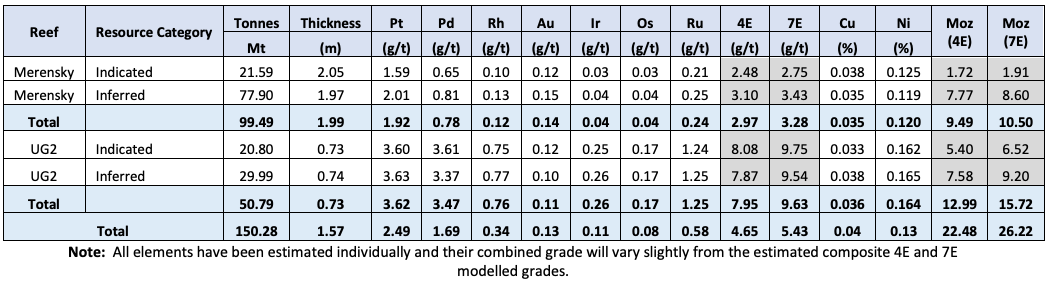

Southern Palladium (ASX:SPD) listed on the ASX in June 2022 with a JORC 2012-compliant Inferred Mineral Resource of 18.8Moz (3PGE + Gold).

You can see that the price of SPD has come down from a high of $1.50 in September 2022 to a low of 27c in August 2023 - it’s currently at 33c. This is despite upgrading their resource to 26.22Moz with 8.4Moz Indicated over this timeframe.

In terms of volume, aside from a heavy trading week post-IPO (which I’ve edited out for clarity’s sake), you can see just how thinly traded this company’s stock is, with most weeks not reaching 200k shares traded.

After a particularly strong couple of years for PGMs, a price spike which had coincided with the Russian invasion of Ukraine was the last hurrah - see where the price touched $3k on the 10-year chart below. The red X is where SPD listed - you can see why the share price has been suffering with palladium dropping to sub $1000/oz this year.

Rhodium suffered during the same timeframe, after going completely bananas between 2016 and 2021, when it did an approximate 25x from $600 to $30k per ounce. It has now come back to earth and seems to have found support at around $4000-4500, which is where it has been since last July.

Platinum hasn’t traded anything like the other two elements in 3PGE, and has essentially remained in a band between $800 and $1200 since 2015 (note though that the previous 10-year period averaged a price of around $1300-$1400).

Financials

Shares on Issue/Market Cap

The company has 87.5m shares on issue, with no raises since the IPO. At 33c per share, this gives SPD a market cap of ~$29m.

There are also 1.2m Performance Rights contingent on achieving a 2Moz 3PGE Mineral Reserve (not resource), and 7.2m options held by directors and the Lead Managers of the IPO raise, with a strike price of 87.5c.

Company Structure

Southern Palladium owns a 70% interest in a South African private company, Miracle Upon Miracle Investments Proprietary Limited (MUM), which owns 100% of the Prospecting Right to the Bengwenyama PGM project. The remaining 30% of MUM is held by the local Bengwenyama community - this type of setup is common in South Africa due to BEE (Black Economic Empowerment) policies.

Cash

The company had $8.3m in cash (as well as another $0.6m held by Miracle Upon Miracle Investments) as of the end of December, which should last five quarters at the current burn rate.

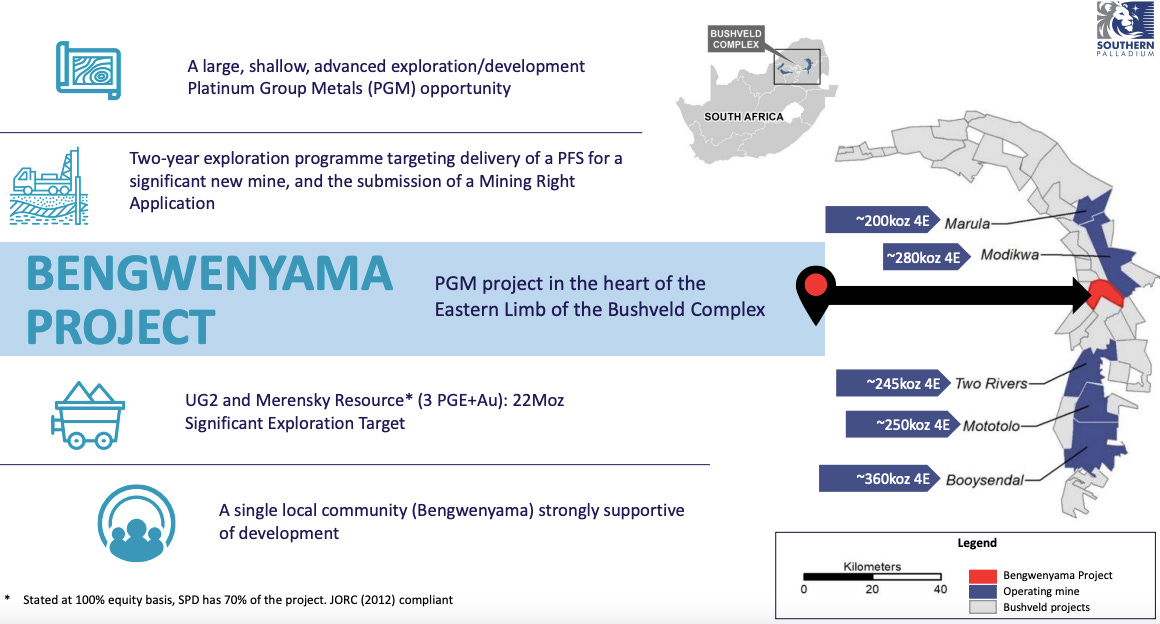

Project

Bengwenyama (70%)

Here’s the fun bit. Bengwenyama is nestled in the Eastern Limb of a Tier 1 PGM mining jurisdiction - the Bushveld Complex - and has various operating PGM mines to the north, east and south.

Note the names of the mines around them in dark blue (you’ll need to squint), and enjoy the comparison here, based on numbers from the project’s Scoping Study, updated last month:

The names around them are some of the biggest names in PGMs as well, including AngloAmerican Platinum (JSE:AMS) and Impala Platinum (JSE:IMP).

As mentioned earlier, in the last couple of years the company has delivered on its plans to thoroughly drill out the resource and progress necessary studies on the project.

These plans (and the project as a whole) are talked through by the Managing Director, Johan Odendaal in these interviews with Crux Investor (a channel that I’m a big fan of, by the way). I definitely recommend giving these a watch. The first is from December 2022, six months after listing:

And the second is from September 2023:

What I inferred from those videos is that the mineralisation, the style of mining, the metallurgy, the processing - it’s all in line with the surrounding, existing, operating mines for the most part, and being in the middle of a prolific mining district, there’s plenty of infrastructure around. As such, I get the feeling that there’s a pretty clear line of sight from where we are now through studies and towards production.

The Bengwenyama project - particularly the UG2 reef as you can see below - is seriously high grade, and with 26.22Moz in total across both reefs (Indicated and Inferred), there’s likely scope for the mine life to extend well beyond what is said in the Scoping Study as more ounces get upgraded to Measured and Indicated. There is infill drilling planned for the second half of 2024, feeding into the PFS.

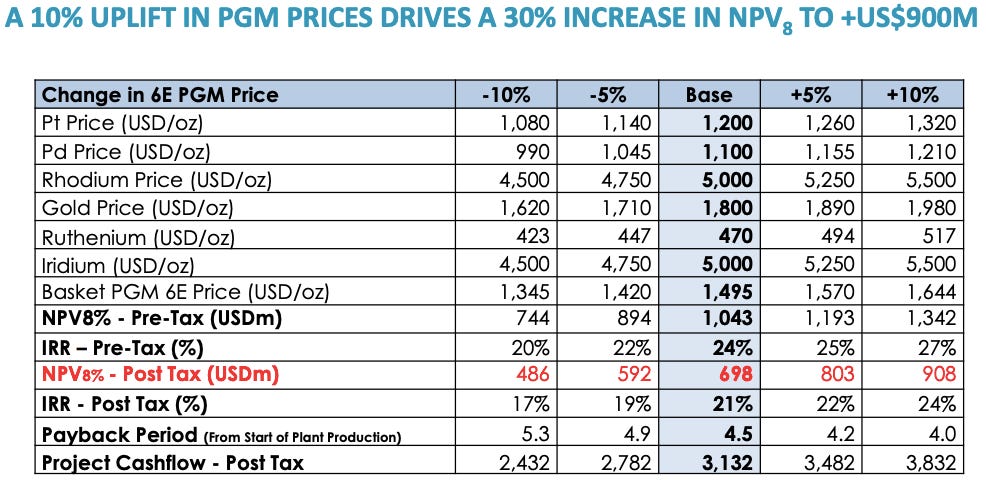

In terms of project economics, here are the numbers/sensitivities from the updated Scoping Study. Current spot prices are below base case assumptions for now, but it shows that even at the -10% scenario (which to be fair, we are still below with platinum prices at around $900/oz) this is still a profitable project to the tune of $486m USD at a discount rate of 8%.

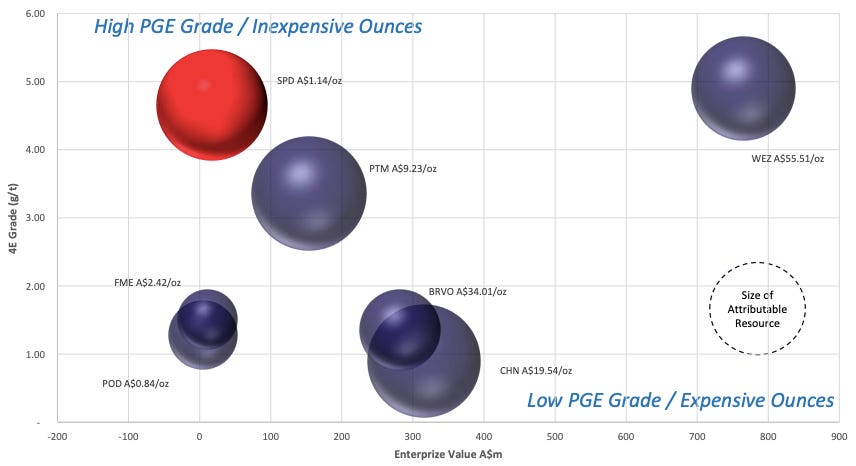

Here’s the AISC curve for PGM producers - see that blue line running along the top? That’s revenue at the spot prices listed below, from December 5th last year. Yup. Wow.

To be honest, I was actually planning on writing about another ASX-listed PGM stock over the weekend, but when I found SPD, I couldn’t help but switch.

The register is tightly held, and with such low volume it’ll be difficult for any bigger fish to put together a meaningful position without pushing the share price higher.

People

Johan Odendaal

Managing Director Johan Odendaal has been working with the Bengwenyama to help them unlock the value of this project since 2006 through his mining consultancy firm, Minxcon. In the Crux interviews above, he briefly describes the legal back and forth that took place throughout this period, but it’s detailed quite well in the company prospectus (section 3.6, pages 35-57). Upon reading that, you get the impression that the relationship between the company and the Bengwenyama is long term and solid.

Worth mentioning as well that Odendaal’s professional background is 100% South African mining, with a focus on PGMs, since the mid 1980s. That’s a lot of time to review a lot of projects, and to think that this company is finally getting moving on this ground specifically after all this time is another positive. Compare this with your fly-by-nights who went from gold, to lithium, to uranium in the course of 3 years, and you’ll see the value that this represents.

Roger Baxter

New Non-Exec Chair as of this year, Baxter gets a great rap for his leadership of the Minerals Council of South Africa from 2015 to 2023. Having previously held senior roles in strategy and economics at the South African Chamber of Mines, as well as a brief stint with Rio Tinto, his involvement would appear to be another boon for the company.

Terrence Goodlace

Most people hide their early jobs on Linkedin - but not former and founding Non-Exec Chair Terrence Goodlace! From what seems like an internship in 1977 to holding various senior roles at Gold Fields from 1998 to 2008, then to CEO of Metorex from 2009 (acquired in 2012), then the CEO of Impala Platinum from 2012 to 2016 - Mr Goodlace was enormously qualified for the role and only stepped down because he was stretched a bit thin, which left him seemingly peeved.

Where to from here?

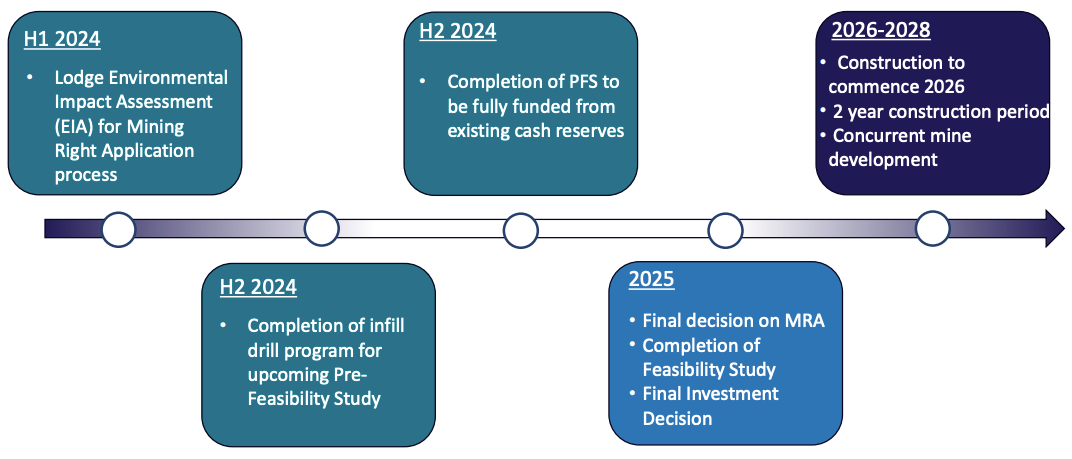

Here’s what it says in the MD’s pack - they’re looking to blow through the PFS, DFS and FID by the end of next year. My guess is that given the five-quarter runway there’s a cap raise coming later this year - if that’s substantial, then it may end up being the last one before a mine is financed and/or a neighbour picks it up.

Given the strong capital support, the calibre of the people involved, the relationships with the landowners, and the grade, I think this one is likely to surprise once people know it exists and/or PGM prices pick up again.

Crickets…!

Disclaimer: This is not financial advice, and I am not a financial advisor. If you are interested in any of the ideas explored by Microcaps Anonymous, you should discuss them with your financial advisor, who will probably chastise you for looking at microcaps in the first place, and they’d probably be right!

Haven’t subscribed yet? Get free posts to your email at least once a week with deep dives into microcap stocks that might just have something to them.

Know someone who shares your passion for microcap stocks? Do them (and me!) a favour and send this post their way!

Good morning,

thank you for your interesting comments. Basically, I agree with you. However, while SPD was unable to show any positive price development, PLG was able to earn the first 40%. How do you see PLG compared to SPD? Thank you and have a nice Sunday. Greetings

IRR 21%, what's good about that? And when I look at the assumed prices...where did they make a wrong turn? And write conservative assumption?

Post-tax NPV of ~USD700 million based on conservative commodity price assumptions (Pt US$1200/oz,

Pd US$1100/oz, Rh US$5000/oz). Platinum is at 920 USD, palladium at 1,000 USD